Introduction – The importance of retirement planning in your 30s

Retirement may seem like a distant dream when you’re in your 30s,But the fact of the matter is when it comes to retirement, early planning now can help set you up for a comfortable and secure future. While making ends meet is important, put some effort into planning your future retirement plans—and how to obtain them. When you start early, you open up the most options. Just think about having a feeling of complete security when you retire: That you’ve already laid the financial foundation long before your final days. It’s time to take action, not just wait. And remember—It’s more than possible for you to turn those thoughts of early retirement into reality!

Understanding your retirement goals and timeline

Understanding your retirement goals is the first step on the path to a secure tomorrow. What exactly do you see yourself doing in older age? Are you dreaming of seeing the world, starting your own business, or indulging in a few favorite hobbies?

Determining when you want to retire plays a decisive role. Do you want an early 60s lifestyle, or perhaps sooner? This decision will serve as the guide to your savings strategy. Everyone should have their own plan but one thing is certain-preparation pays off.

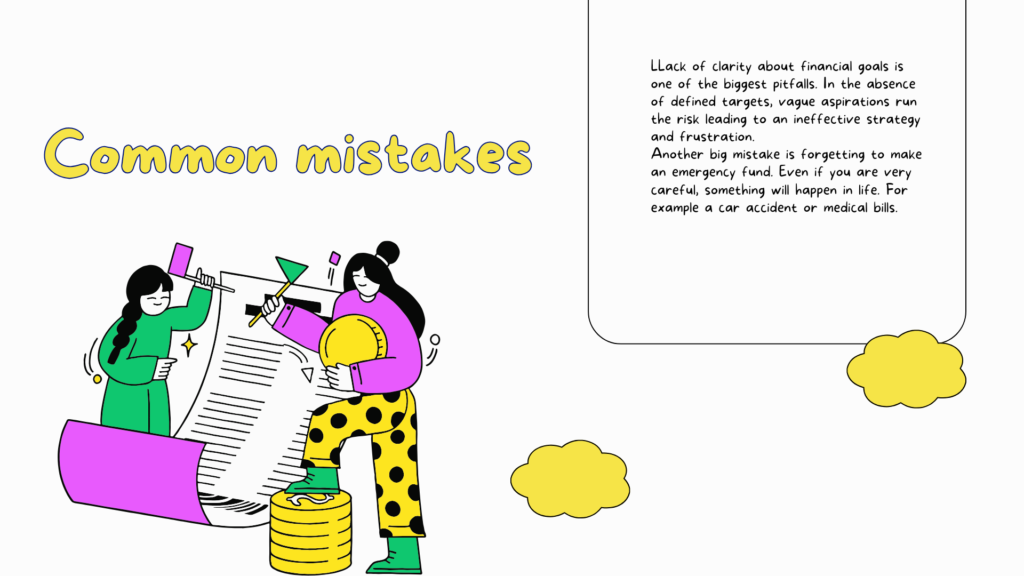

Be realistic about what kind of lifestyle you want-after all there are many beautiful, fascinating, nurturing and delightful experiences waiting in the wings. “So “Too soon” is not really an option unless it means dying early. And figure out just how much money, each year, it is going to cost for you to live in retirement. That includes costs like housing and health care plus leisure pursuits of various kinds.

Assessing your current financial situation

Before starting the journey to retirement, it is critical to understand where you are financially. You have to begin by surveying your income sources and expenses. At least a month should be the period of time where everything that comes in and goes out is tracked on a daily basis.

Next ball-park the size of your outstanding debts. This could cover credit cards, student loans or mortgages- anything on which you owe money. These will then need to have their debts serviced at minimum cost and with minimal strain over time.

Review any savings accounts and investments that could be used towards retirement savings. Henceforth when evaluating your traditional savings accounts or employer sponsored plans such as 401(k) s, take stock of the balances.

Understanding these factors will help you see how much can be set aside for retirement a month. This step lays the groundwork for wise decisions as you plan towards long-term financial health.

Creating a budget and setting aside money for retirement savings

So, the first step in preparing for your retirement is to get a budget together. To begin the process: Write down all monies coming in. Take a notebook and jot down everything from your last payroll stub, pension check or Social Security statement into that book A month later, compare planned expenses with actual achievements. Put another way, where did one plan that they wouldn’t spend X dollars and actually spend Y instead? This work will show you just how many of the things which seem innocent can really add up to be quite a bite out of your wallet over time.

Secure and enjoyable futures don’t just happen. producing a monthly financial results sheet will show to you what exactly time is turning as it passes in terms of day to day living costs Then, start cutting back on “extras.” To be sure, idle subscriptions–have you ever read the magazines you subscribe to in detail as long ago?–can come in for pruning. Likewise, if dining out happens more than twice a week with more money than you want to spend at each food transaction then soon or an extra $1,000 monthly might find its way into the pockets of restaurateurs and others who need it a great deal less than I do.

Once your budget is finished, concentrate on the retirement portion. Try putting at least 15% of your income into savings each month.

This process is made easier by using automation. So right after a payday, have this done automatically as follows: Transfer an amount equal to 20% of whatever take home pay you receive in cash or checks to your personally chosen retirement accounts. This eliminates all effort of having to set aside funds.

It doesn’t matter how small you start. All the little contributions add up through compound interest over time so that eventually–even with high investment returns from there onward–one day those dinky dollar fling doings could become life-gate opening ceremonies in their magnitude!

Exploring different retirement savings options (401k, IRA, etc.)

When it comes to retirement savings options, there’s a wealth of choices available. Understanding these can significantly impact your future comfort.

A 401(k) plan is popular for its employer contributions. Many companies match a percentage of what you put in, essentially giving you free money. This option makes saving easier and more rewarding.

IRAs, or Individual Retirement Accounts, come in two flavors: traditional and Roth. With a traditional IRA, tax benefits are enjoyed upfront while withdrawals during retirement may be taxed. A Roth IRA allows for tax-free withdrawals later on but requires after-tax contributions.

Self-employed individuals have unique avenues as well. SEP IRAs offer higher contribution limits compared to standard IRAs, making them an attractive choice for those with fluctuating incomes.

Each option has its pros and cons; it’s essential to assess which aligns best with your financial situation and goals.

Taking advantage of employer matching programs

Employer matching programs are an opportunity you shouldn’t overlook. Taking the full advantage of your company’s generosity with its retirement accounts can be very valuable .Many firms offer a 401(k) that not only matches but in some capacity even outpaces with investment beyond what could possibly be accumulated through individual action by him alone. This is money for the pickings.

When you contribute to your retirement savings, you’re not just saving for the future. This means that your employer has also increased the return on these investments by the contributions they make to match them at percentages such as these: If they match 50% of your contributions up to 6%, this adds real value over time.

It’s an easy way to save – without squeezing your budget too hard Make sure you’re contributing enough to at least meet the company’s maximum match

Be sure to keep aware of the limitations on benefit programs. Each company sets its own rules, yet at all costs understanding these programs will squeeze out the most in favor of yours that they offer.

Enroll as soon as possible. The more dollars saved, the sooner you can retire.

Considerations for investing in stocks, real estate, and other assets

Investing in stocks can be a good way to increase the money you have saved for retirement. Pick a few solid companies with strong track records

Real estate is another potentially lucrative investment opportunity. It’s widely seen as being secure, especially if you go for rental properties or REITs (Real Estate Investment Trusts). These will eventually pay for themselves in passive income and at the same time build up equity.

Branch out into assets you may not have considered before, such as gold or Bitcoin. While they carry risk, they will help to diversify your portfolio very effectively indeed.

Always investigate your risk capacity before embarking on any investment mission.

A different kind of investment discipline Investment priorities can be tailored to suit your own objectives and time scale. In Alternatively, make regular checks and adjustments based on performance and the changing current in the financial world.

Importance of diversifying your retirement portfolio

It is an important strategy to spread risk in your retirement savings. Depend at all on one type of investment, and market out fluctuations should assuredly be your fate. Yet with investments in these different assets, spread out among stocks, bonds and real estate; you have effectively created a barrier against the ups and downs of individual markets.

Each kind of investment responds to economic conditions in its own way. For instance, while stocks may roar ahead during a bull market they will suddenly plummet in times of sea change. Real estate as its household name remains stable and tends to grow with time.

Adding alternative investments such as index funds and precious metals can further strengthen resilience. These assets typically show low correlation with traditional markets.

It’s important to remember that diversification isn’t just about variety; it’s also about balance. By regularly reconsidering your portfolio, you’ll be in tune with changing financial goals and market trends. This proactive approach ensures security both for now and later in your early retirement plans.

Reassess

As you navigate your 30s, it’s crucial to reassess your retirement strategy regularly. Life changes quickly—new jobs, family dynamics, and financial circumstances can all impact your planning. Set aside time annually to review your goals, savings rate, and investment performance.

Seek out updated information or insights on early retirement forums where members share their experiences. Consider adjustments based on market trends in stocks or real estate as well as new opportunities for self-employed individuals regarding retirement accounts like SEP IRAs or health savings accounts.

Your approach should be flexible yet focused. Monitor how different assets perform over time; long-term investments such as index funds or even crypto may shift in relevance depending on economic conditions. Regular assessments ensure that you’re not only prepared but also optimizing the resources at hand for a comfortable future.

Remember that successful retirement planning is an ongoing process. Stay informed and proactive about both your financial landscape and personal aspirations related to early retirement today.